Why Retail Store Owners Can't Afford to Skip Public Liability Insurance

Introduction to Public Liability Insurance for Retailers

The high cost of negligence claims and how it impacts your business

Facing a negligence claim can be daunting and the financial repercussions can escalate quickly. Legal fees, compensation payouts, and the indirect cost of reputational damage can threaten the very existence of your retail store. In today's litigious society, a single incident can lead to staggering costs that have the potential to cripple your business finances, emphasizing the critical nature of being adequately insured.

Understanding the basics: What does public liability insurance cover?

Public Liability Insurance is designed to protect business owners like you from the financial strain of these scenarios. It covers the compensation costs associated with injury to a third party or damage to their property that occurs in the course of a business’s operations. The policy ensures that should an unforeseen event happen, your store can continue to thrive without the burden of crippling financial obligations.

In summary, Public Liability Insurance is not just an option; for retail store owners, it's a protective layer that safeguards businesses against unpredictable human and property risks. Without it, you are leaving your business vulnerable to claims that could have otherwise been mitigated with the right coverage.

Not An Option, But A Necessity

In the bustling environment of a retail store, accidents are not a matter of if, but when. Public Liability Insurance ceases to be just another line item on your budget—it becomes an indispensable part of your business operations. As a retail store owner, you are not just selling products; you are also ensuring the safety of everyone who steps through your doors.

Why public liability insurance is crucial for your retail store

The crucial nature of Public Liability Insurance lies in its ability to safeguard your business from financial disasters. Without this cover, you are personally accountable for any legal costs or compensation claims. These could arise from a range of incidents, from accidental damage to a customer’s property to more severe cases where someone is injured on your premises. For a small business, these costs can be the difference between thriving and bankruptcy.

It also plays a key role in protecting your reputation. Customers trust businesses that are insured, understanding that they are protected should anything go wrong. This trust is an invaluable asset in today’s competitive retail landscape.

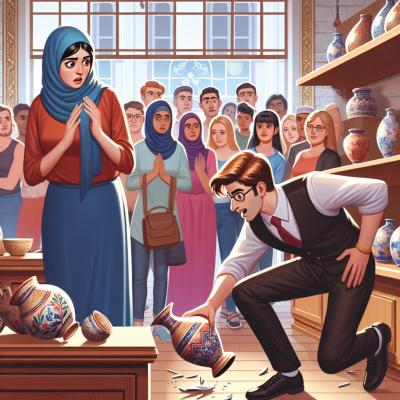

Scenarios where insurance can save the day

Imagine a child knocking over a display cabinet, resulting in injury, or a customer slipping on a freshly mopped floor. In both scenarios, your Public Liability Insurance is your financial shield. It covers you for the compensation you may have to pay for their injuries, as well as any associated legal fees. This kind of coverage ensures that these everyday risks do not turn into financial nightmares.

Consider a retailer faced with a hefty lawsuit from a customer injury caused by falling merchandise or an electrical fire that leads to property damage claims from neighboring shops. Both situations, while differing in severity, underscore the value of Public Liability Insurance, preserving both the financial health and continuity of your store.

Taking into account these scenarios, it’s clear that forgoing Public Liability Insurance puts more at stake than just the physical premises of your store—it places your entire livelihood at risk.

The Cost of Being Uninsured

One of the most persuasive arguments for retail store owners to secure Public Liability Insurance is the staggering cost associated with being uninsured. It's an unfortunate reality that the expenses which arise from an accident or injury claim can eclipse the annual cost of an insurance premium several times over.

Comparing the cost of insurance vs. potential legal fees and compensation payments

When you consider the potential financial ramifications of a legal battle, the cost of an insurance policy is paltry in comparison. Legal defense fees alone can mount quickly, even before compensation is awarded to a claimant. With just one significant claim, a retailer might be responsible for tens, if not hundreds, of thousands in compensation—it's not hard to see how operating without insurance is a gamble with unfavourable odds.

Comparatively, the consistent payment of an insurance premium gives you peace of mind and stability in your financial planning. It acts as a predictable expense that prevents the unpredictability of massive, claim-induced financial hits. In essence, paying for Public Liability Insurance is a strategic investment in your business's resilience.

The hidden costs of not having public liability insurance

Beyond the visible costs like legal fees and compensation, there are hidden costs of being uninsured. An incident that leads to a claim can have a ripple effect, leading to increased insurance premiums in the future, interruption of business activities, and even a tarnished reputation which can deter potential customers.

An uninsured incident can also strain relationships with suppliers and partners, should they feel their interests are at risk. What's more, the stress and distraction of managing a crisis without insurance support can take a toll on you and your team, impacting daily operations and the overall health of your business.

Hence, while an insurance premium is a tangible expense, the intangible costs of being uninsured—both in potential financial terms and the wellbeing of your business—make it an expense that cannot reasonably be ignored. Public Liability Insurance is not just a cost; it's a critical investment in protecting and future-proofing your retail business.

How Public Liability Insurance Protects Your Business and Assets

Securing your retail store's financial health against claims

The primary role of Public Liability Insurance in your retail business is to fortify its financial health against claims that could otherwise be disastrous. In the event of a lawsuit or demand for compensation due to injury or property damage caused within your premises or by your business activities, this insurance serves as a bulwark, absorbing the financial shock such claims may generate.

Without this critical layer of defense, the cost of compensating damaged parties, as well as the associated legal fees, would directly affect your store's finances. This is particularly relevant for small and medium-sized businesses where such unexpected expenditures can mean the difference between solvency and bankruptcy. With Public Liability Insurance, however, retail owners can transfer this significant risk to the insurer, ensuring business continuity even in the face of adversity.

Protecting your business’s reputation in times of crisis

Beyond mere financial protection, Public Liability Insurance acts as a safeguard for your business’s reputation during times of crisis. When accidents occur, the response of your business is often scrutinized by the public and media. Having insurance not only demonstrates a professional and proactive approach to civic responsibility but also assures your customers that they are engaging with a business that is diligent about their welfare and ready to address any unfortunate incidents competently.

A good reputation is hard-earned and is an invaluable asset, especially in retail where trust plays a pivotal role in customer loyalty. By ensuring that claims are handled efficiently and fairly by your insurance provider, you minimize any negative fallout and maintain the integrity and reputation of your business. This reassurance bolsters customer confidence and contributes to a positive perception of your brand, which can be essential to your survival and growth in a competitive market.

Public Liability Insurance, in essence, comes to the forefront when protecting the assets of your business, both tangible and intangible. It provides a stable foundation that enables you to operate with assurance, knowing that your store's financial health and reputable standing are shielded from the potentially damaging impacts of liability claims.

The Process of Getting Public Liability Insurance

How to choose the right insurance policy for your retail business

Selecting the right Public Liability Insurance policy requires careful consideration of various factors including coverage details, insurer reliability, and how the policy fits into the unique needs of your retail business. Start by evaluating the nature of your retail operations and the potential risks involved. High foot traffic locations, for example, might demand a policy with higher coverage limits.

You should compare policies offered by different insurers to determine which offers the best balance of coverage and cost efficiency. Look for insurers with a proven track record of handling claims swiftly and fairly. Consulting with industry peers or professionals like insurance brokers can also provide insights into the best policies tailored to retail businesses similar to yours.

Understanding the terms: premiums, coverage limits, and exclusions

It's essential to understand the specific terms of the policies you’re considering. Premiums are the regular payments you make for your insurance cover. These vary according to the risk factors of your business, such as its size and location, the products you sell, and your claims history. Coverage limits are the maximum amounts an insurer will pay out for a single claim or set of claims; ensuring these are sufficient to cover potential damages is crucial.

Equally important are the policy exclusions, which outline what is not covered. This can include intentional damage or contractual liabilities. Understanding these will help you assess whether you might need additional endorsements or separate policies to fill any gaps in coverage. These policy details are not just legalese; they are the roadmap to knowing exactly what protection you’re paying for and what areas could present out-of-pocket risks for your retail business.

When Public Liability Insurance Made All the Difference

Public Liability Insurance proves its worth in practice, as evidenced by numerous retailers who have faced potential financial ruin due to accidents and claims. In one case, a home appliance store owner experienced a customer slip on a spilled liquid in an aisle, resulting in severe back injury. Thanks to their Public Liability Insurance, the subsequent claim was handled smoothly, covering medical expenses and legal fees without impacting the store’s finances.

Another case involved a bookstore where a shelving unit collapsed, narrowly missing a customer but damaging costly personal property. The insurance not only covered the replacement of the damaged items but also shielded the owner from an expensive lawsuit that could have followed.

Lessons learned and what could have happened without coverage

These stories highlight critical lessons for retail business owners. The most resounding is the importance of having the right insurance in place before an incident occurs. Retailers have learned that accidents are unforeseeable and can happen regardless of how many precautionary measures are in place. They underscore that the cost of an insurance premium pales in comparison to the potentially devastating financial consequences of lawsuits and claims.

Without coverage, the appliance store could have faced a dire financial crisis, with the owner potentially losing their business and facing personal bankruptcy. The bookstore's situation could have similarly escalated into a legal quagmire, depleting their resources and souring community relations.

In both cases, Public Liability Insurance provided not just financial safeguarding, but also peace of mind and the ability to continue trading without the added stress of a financial catastrophe looming overhead. These real-life examples are a strong testament to the protective power of Public Liability Insurance for retail businesses.

Addressing common questions and misconceptions

A plethora of questions surround Public Liability Insurance, especially for new or small retail store owners. One prevalent misconception is that this type of insurance is only for larger businesses—this couldn't be more inaccurate. No matter the size of your retail operation, the public interaction inherent to your business necessitates protection against liability claims.

Another common question is about the cost and whether it is affected by the types of products sold. While the nature of your products can influence premiums due to varying risk levels, insurers also consider other factors such as your business location, the number of employees, and past claims history. Understanding that insurance costs are relative to your specific business risks is important when evaluating policies.

Business owners also often wonder whether they need additional insurances alongside public liability. While Public Liability Insurance covers third-party injuries or property damage, it's crucial to understand that it does not cover everything, such as professional negligence or employee injuries, which would require separate policies like professional indemnity and workers' compensation insurances.

It is equally important to know what happens if your business grows or changes direction. While your current policy may provide adequate coverage now, be sure to communicate any significant changes in your business model, product lines, or services to your insurer to ensure you continue to have suitable and sufficient coverage.

Tips for policy management and staying covered

Effectively managing your Public Liability Insurance policy is critical to staying covered. First and foremost, keep your policy documents in a secure yet accessible place, and know your renewal dates to avoid lapsed coverage. Set reminders if necessary as insurance is not retroactive; it only covers incidents that occur while the policy is active.

Review your policy at least annually to ensure that coverage still aligns with the scale and nature of your retail operations. This is especially true as your business grows or changes—the last thing you want is to find your coverage lacking when you need it most.

Keeping accurate records of all incidents, no matter how minor, is also advisable. Should a claim be made, detailed records can be vital in supporting your position. It's an added layer of security that can make a significant difference in the handling of claims.

Lastly, engage with your insurance provider regularly. Good communication can not only help you to better understand your coverage but can also provide your insurer with the necessary insights to tailor your policy to your unique business needs, ensuring the most robust protection for your retail store.

Conclusion: The Investment in Safety and Peace of Mind

We've navigated through the multifaceted landscape of Public Liability Insurance, establishing its paramount role for retail store owners. It's been made evident that such a policy is more than a mere formality; it is an investment in the safety and sustainability of your business.

The scenarios outlined serve as a reminder of the constant risks retail environments are exposed to and the significant protection Public Liability Insurance offers. Not only does it shield your business financially, but it also preserves your hard-earned reputation, provides peace of mind, and endorses a message of responsibility to your customers.

Why securing the right coverage should be a priority

As a retail store owner, you're not just managing operations; you're actively handling risks every day the doors are open. Realistically, even with the most meticulous safety measures, incidents can still occur, and the ramifications without proper insurance are too severe to ignore.

In today’s competitive and litigious environment, taking the step towards securing the right Public Liability Insurance coverage is not just advisable, it's essential. Your business deserves the protection needed to thrive without the looming threat of a financial catastrophe due to unforeseen events.

Taking action to safeguard your business

If you haven't yet done so, let this be the impetus for you to evaluate your current insurance policy or to start the process of obtaining one. Consult with professionals, compare policies, and make an informed decision to protect your store. Remember to review and update your policy regularly, keeping pace with any changes in your business scale or scope.

The journey of securing and maintaining the right Public Liability Insurance is a proactive step towards safeguarding your livelihood. When you're covered adequately, you assure not just the financial stability and operational continuity of your store but also demonstrate a commitment to the well-being of your customers and employees.

With Public Liability Insurance, you're not just covering a potential expense, you're building a foundation for a resilient and trusted business. So, take those steps, secure your coverage, and move forward with the confidence that you have the necessary safety net in place.

Published: Wednesday, 25th Dec 2024

Author: Paige Estritori